How To Finance Your Land Purchase on Vancouver Island, A Practical Guide For Serviced Lots and New Builds

The right financing structure for a land purchase and new build saves time, reduces stress, and keeps costs predictable. Here is how it actually works.

Financing a land purchase and new build on Vancouver Island is not the same as getting a mortgage on an existing home. The product is different (a construction draw mortgage, not a standard mortgage), the approval process involves more documentation, and the way money flows – in stages based on construction milestones rather than in a lump sum at closing – requires active management. This guide covers how the financing actually works for a serviced lot purchase and new build, with specific detail relevant to Jubilee Heights in Campbell River.

Land Loan vs Construction Mortgage: Which One Do You Need?

| Factor | Land Loan | Construction (Draw) Mortgage |

| Purpose | Buy land before you’re ready to build | Fund the build in stages – typically used when builder is engaged |

| When it applies | Raw land, or serviced lot with a longer pre-build horizon | Serviced lot with builder contracted and permit in process |

| How funds are released | Lump sum at land purchase | In stages (draws) after lender inspection at each milestone |

| Collateral | Land only | Land plus completed improvements as build progresses |

| Typical rate | Higher than prime-rate mortgages – land is less liquid collateral | Closer to residential mortgage rates once build is underway |

| Duration | Short-term bridge – 1–2 years typically | Converts to standard amortizing mortgage at occupancy |

| Best fit for | Raw land buyers, or buyers with a longer pre-build timeline | Serviced lot buyers with builder engaged and timeline defined |

Practical rule of thumb: if you have a serviced lot and a builder ready to start, move directly to a construction draw mortgage and minimise time on a land-only loan. The interest rate differential and the administrative overhead of bridging from a land loan to a construction mortgage is worth avoiding if your timeline allows.

Why Serviced Lots Are Easier to Finance

Lenders assess construction financing risk primarily through two lenses: how clearly can they appraise the finished asset, and how predictable are the construction costs and timeline. A serviced lot at Jubilee Heights in Campbell River answers both questions well.

The appraisal is straightforward because the community is established, comparable sales exist, and the infrastructure (roads, services, utilities) is already complete – not contingent on future development. The construction cost prediction is cleaner because there are no servicing unknowns: connection points are mapped, hook-up fees are known, and off-site work is not required.

The result: serviced lot construction mortgages typically require 10–15% contingency vs 20–30% for raw land, progress faster through underwriting, and require less pre-approval documentation.

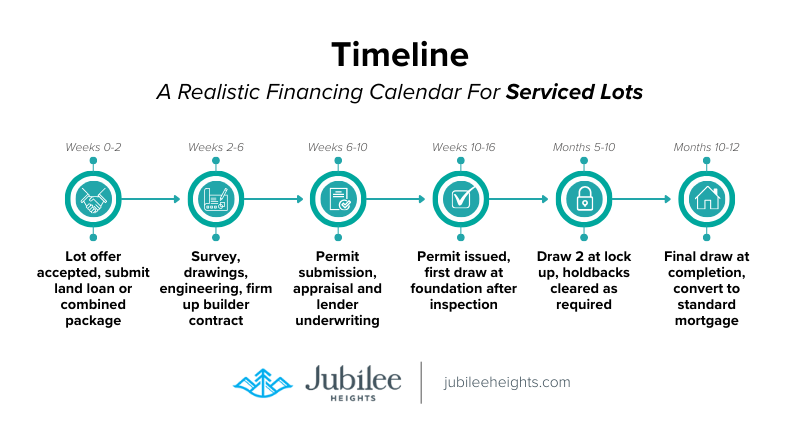

How a Construction Draw Mortgage Works

A construction mortgage holds the approved funds and releases them in stages (draws) after a lender-appointed inspector confirms each milestone is complete. You pay interest only on funds that have been advanced – not on the full approved amount.

| Stage | Funding Release | What It Confirms |

| Land purchase | Your down payment and any land loan | Lot title transfers to you |

| Foundation complete | Draw 1 – after lender inspection | Typically 25–35% of construction budget |

| Lock-up complete | Draw 2 – after lender inspection | Framing, roof, windows, and exterior doors complete |

| Completion (occupancy) | Final draw – after lender inspection | Substantially complete, occupancy permit issued |

| Post-completion | Convert to standard amortizing mortgage | Fixed or variable rate mortgage term begins |

The inspection at each stage is conducted by a lender-appointed appraiser, not your builder’s inspector. Keep documentation organised – drawings, invoices, change orders, and photos – to support a fast inspection turnaround. Delays in documentation submission are the most common cause of draw delays, which add interest cost and slow your builder’s cash flow.

What to Bring to the Lender: The Complete Document Package

Lenders approve construction mortgages based on the strength of your documentation package. A complete package submitted at first application moves significantly faster than an incomplete one that triggers multiple information requests.

- Government-issued ID and income verification (T4s, NOAs, or self-employment financials for the past 2 years)

- Lot purchase agreement and deposit confirmation

- Architectural drawings, elevations, and specifications

- Structural engineering and, where required by the City, energy calculations

- Builder contract – ideally fixed-price or clearly scope-defined with listed allowances

- Itemised construction budget with allowances explicitly listed and a contingency line

- Current permit application status or expected submission date

- Course of construction insurance confirmation

- Current mortgage statements if carrying another property

For Jubilee Heights lots, Couverdon’s sales team can provide the servicing summary, lot plan, and community documentation that supports the appraisal portion of your application.

Down Payment: What to Budget

Construction mortgage down payment requirements vary by lender and by the total loan-to-value ratio of land plus construction. As a planning baseline for a serviced lot in Campbell River:

- Conventional construction mortgage (no default insurance required): typically 20% of the total project cost (land + construction)

- High-ratio construction mortgage (below 20% equity): requires mortgage default insurance through CMHC, Canada Guaranty, or Sagen – available on new builds up to CMHC’s applicable purchase price limit

- Down payment on the land component specifically: if taking a land loan first, expect 25–35% of the lot price

The cash costs beyond the down payment that buyers most commonly underestimate: Property Transfer Tax (1% on first $200,000 of lot price, 2% on the balance up to $3M), legal and notary fees, lot hook-up fees paid to the City of Campbell River at permit stage, course of construction insurance, and the 10–15% contingency that should be in your budget.

Rate Holds, Bridge Financing, and Carrying Costs

A rate hold locks your construction mortgage rate for a specified period – typically 90 to 180 days. If your build is expected to span longer than the rate hold, ask about extension options at application. Rate hold requirements and extension terms vary significantly between lenders.

If you are selling a current property while building, bridge financing covers the overlap period between taking possession of the lot and receiving proceeds from your sale. Most lenders offer bridge financing as an add-on to the construction mortgage. Confirm the bridge period length, rate, and what documentation triggers the bridge advance.

Carrying costs during construction – interest on funds advanced, inspection fees, insurance – add up over a 10–12 month build. Budget approximately 0.5–1.0% of the total construction value in carrying costs for a standard Campbell River build timeline.

Working With Local Lenders on Vancouver Island

Vancouver Island credit unions – including Coastal Community Credit Union and First West Credit Union – have experience with construction files on the Island and often move faster than national banks on local projects. They understand the Campbell River market, know local appraisers, and can be more flexible on construction schedule variations than national lenders working through centralised underwriting processes.

National banks offer broader product menus, longer rate holds, and sometimes more competitive rates on the construction-to-term conversion. An independent mortgage broker can compare both options and present the tradeoffs with specific numbers, which is worth the effort on a file of this size.

Ready to Talk Numbers?

→ View available Phase 5 and Phase 6 lots at Jubilee Heights

→ Read the complete building guide for Campbell River

→ Talk to our team about lot availability and builder referrals

FAQs

Can I finance a land purchase and construction together on a single mortgage?

Yes. Many lenders structure a combined package that starts with the lot purchase and then advances funds in construction draws. This avoids the cost and administrative overhead of bridging from a separate land loan to a construction mortgage. For serviced lots with an engaged builder, this is typically the most efficient structure.

Do I pay interest on the full construction mortgage from day one?

No. During construction you pay interest only on the funds that have been advanced (drawn). If your approved construction mortgage is $600,000 but only $150,000 has been advanced after the foundation draw, you pay interest only on the $150,000. Interest on the full amount begins when the mortgage converts to a standard term at completion.

What is mortgage default insurance and does it apply to new builds?

Mortgage default insurance (through CMHC, Canada Guaranty, or Sagen) is required when the loan-to-value ratio exceeds 80% – meaning less than 20% down payment. It applies to new construction up to CMHC’s applicable purchase price limit. The insurance premium is added to the mortgage and amortised over the mortgage term. Lenders require proof of coverage before advancing the first construction draw.

What if my construction costs exceed the approved budget?

Budget overruns are handled through a change order process. If costs exceed the approved construction budget, you have three options: bring additional cash to close the draw gap, request a budget revision from the lender (which requires re-underwriting and may require an updated appraisal), or reduce scope to stay within the approved amount. The best protection is a complete and conservative budget at application, with a realistic contingency.